On May 27, 2024, the Ministry of Finance issued the "Corporate Sustainability Disclosure Guidelines - Basic Guidelines (Draft for Comments)" (hereinafter referred to as the "Basic Guidelines" Draft for Comments) and solicited public opinions, marking the beginning of the construction of a unified national sustainable disclosure standards system, which will guide and regulate corporate behavior and promote the comprehensive and sustainable development of the economy and society.

Drafting Background

At present, environmental, social and governance (ESG) issues have become an indispensable part of corporate operations, investment decisions and regulatory policies around the world. At present, some regions and enterprises in my country have started sustainable information disclosure practices, but there is still a lack of unified standards internally. At the same time, relevant international standards have been introduced one after another. The dual pressures from both inside and outside have prompted my country to speed up the formulation of unified and comparable sustainable disclosure standards to adapt to international trends and strengthen China's positive role in global sustainable development governance.

The Ministry of Finance, together with relevant departments, organized experts to conduct a three-month assessment of the applicability of international standards in China, and carried out a series of research projects, exchanges and discussions. Adhering to the overall idea of "actively learning from, focusing on China, absorbing all, and highlighting characteristics", the draft of the Basic Standards for discussion and comments was formed. The draft of the Basic Standards for comments aims to propose a unified national sustainable disclosure standard that reflects the beneficial experience of international standards, conforms to China's national conditions and can highlight Chinese characteristics.

Main content

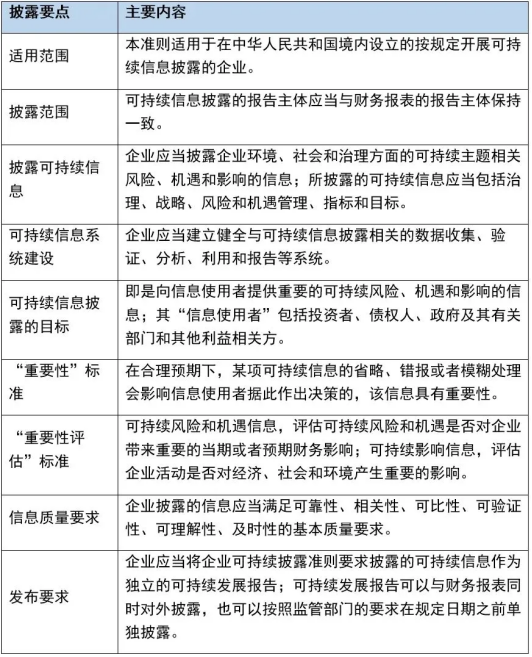

The "Corporate Sustainability Disclosure Standards - Basic Standards (Draft for Comments)" released this time is based on the general requirements for disclosure of sustainable financial information (hereinafter referred to as "S1"), and proposes the framework of a unified national sustainable disclosure standard system. The unified national sustainable disclosure standard system consists of basic standards, specific standards and application guidelines. In terms of content, the draft for comments on the "Basic Standards" is generally consistent with the international standard S1 in terms of information quality characteristics, disclosure elements and related disclosure requirements; it makes provisions based on China's actual situation in terms of purpose, scope of application , disclosure objectives, materiality standards, format structure and some technical requirements.

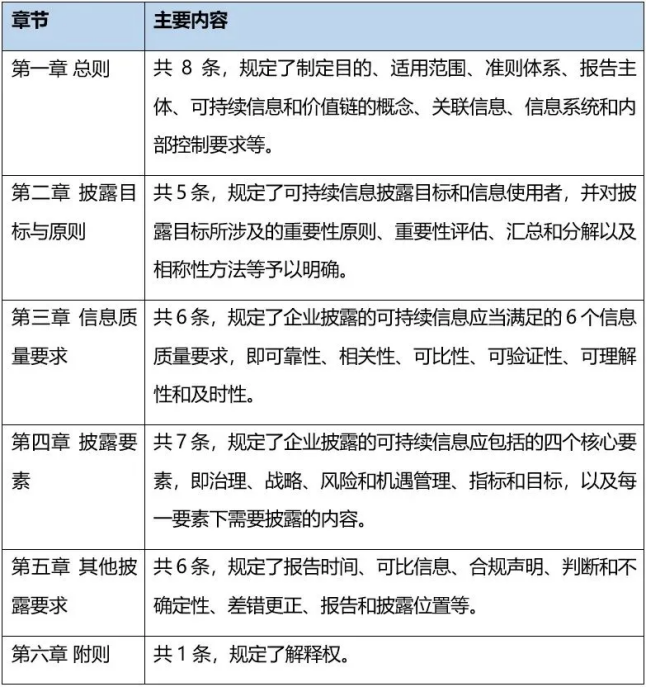

The draft for soliciting opinions on the Basic Guidelines consists of six chapters and 33 articles. The main contents are as follows:

Key points

Green Gold Summary

(I) The draft of the Basic Standards has initially established the framework of a unified national sustainable disclosure standards system.

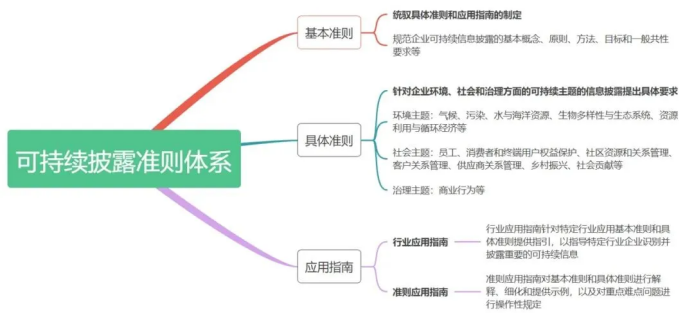

In terms of the disclosure standards, the draft for comments on the Basic Standards, based on the conclusion of the previous assessment of the applicability of international standards in China, and considering that S1 is a general disclosure requirement, only provides for the disclosure of sustainable information in principle. This institutional arrangement is conducive to the formulation and implementation of specific standards, and is also conducive to the convergence of China's sustainable disclosure standards with international standards. The national unified sustainable disclosure standards system consists of basic standards, specific standards and application guidelines:

The basic guidelines regulate the basic concepts, principles, methods, objectives and general requirements for corporate sustainable information disclosure, and govern the formulation of specific guidelines and application guidelines.

The specific guidelines put forward specific requirements for the disclosure of information on sustainable themes in the environment, society and governance of enterprises. Environmental themes include climate, pollution, water and marine resources, biodiversity and ecosystems, resource utilization and circular economy, etc. Social themes include protection of rights and interests of employees, consumers and end users, community resources and relationship management, customer relationship management, supplier relationship management, rural revitalization, social contribution, etc. Governance themes include business behavior, etc.

Application guides include industry application guides and standard application guides. Industry application guides provide guidance on the application of basic standards and specific standards for specific industries, so as to guide enterprises in specific industries to identify and disclose important sustainable information. Standard application guides explain, refine and provide examples for basic standards and specific standards, and make operational provisions for key and difficult issues. In addition, in order to solve problems that arise in the process of enterprises implementing sustainable disclosure standards, standard implementation questions and answers are provided when necessary to improve the comparability and transparency of sustainable information and promote the application of sustainable disclosure standards.

(II) The draft of the Basic Standards puts forward clear planning objectives for the establishment of a sustainable disclosure standards system.

The overall goal is that by 2027, China's basic sustainable disclosure standards and climate-related disclosure standards will be issued. By 2030, the country's unified sustainable disclosure standards system will be basically established. In view of the long construction cycle of the standards system, relevant departments can first formulate disclosure guidelines and regulatory systems for specific industries or fields according to actual needs, and gradually adjust and improve them in the future. In the future, China's corporate sustainable information disclosure system will move towards integration and standardization, provide strong support for China to establish a comprehensive and systematic ESG system, and help improve the international competitiveness and market influence of Chinese companies.

(III) The draft of the Basic Guidelines has established an information disclosure framework that complies with international trends and is in line with China's national conditions.

In terms of following international trends, the draft of the Basic Standards integrates the internationally accepted four-element framework of "governance, strategy, risk and opportunity management, indicators and targets" to provide a clear structure for corporate sustainable information disclosure. In addition, the draft of the Basic Principles also continues the "dual importance principle" emphasized in the international and domestic sustainable development disclosure guidelines of the Shanghai, Shenzhen and North Stock Exchanges, requiring companies to assess whether sustainable risks and opportunities have important current or expected financial impacts on the company and whether corporate activities have important impacts on the economy, society and the environment in combination with the requirements of the specific applicable corporate sustainable disclosure standards.

In terms of adapting to China's national conditions, the draft of the Basic Standards also maintains a certain degree of flexibility and practicality, allowing companies to make appropriate disclosures based on their own resources and capabilities on the premise of complying with basic requirements, thereby reducing the disclosure burden and additional costs of companies; in terms of specific standards, the social issues clearly propose sustainable issues with more Chinese characteristics, such as "rural revitalization" and "social contribution", to make good international connections, reflect Chinese characteristics, and further facilitate the convergence of China's sustainable disclosure standards with the ISSB standards.

(IV) The draft of the Basic Guidelines pays more attention to the needs of diverse information users.

In terms of paying attention to the needs of diversified information users, the draft of the Basic Standards clearly aims to meet the needs of diversified information users for sustainable information disclosure. It not only meets the needs of investors and creditors targeted by international standards, but also covers a wider range of information needs for the government, its relevant departments and other stakeholders.

(V) The draft Basic Guidelines require enterprises to standardize sustainable information data management and improve the quality of information disclosure.

In terms of information collection and management, the draft of the Basic Guidelines requires companies to standardize systems for data collection, verification, analysis, utilization and reporting related to sustainable information disclosure. By promoting companies to establish and improve data management systems and indicator systems suitable for their own management and development, the transparency and effectiveness of companies in sustainable information disclosure will be further improved, thereby ensuring the quality of information disclosure.

(VI) When implementing the draft Basic Guidelines, my country's national conditions will be taken into consideration, and a strategy of classified implementation and gradual advancement will be adopted.

In formulating implementation strategies, the draft for comments of the Basic Standards comprehensively considers the development stage and disclosure capabilities of Chinese enterprises, and clearly points out that a "one-size-fits-all" mandatory implementation requirement will not be adopted in the implementation strategy. In the future, a strategy of distinguishing priorities, piloting first, and advancing step by step will be adopted, expanding from listed companies to non-listed companies, from large enterprises to small and medium-sized enterprises, from qualitative requirements to quantitative requirements, and from voluntary disclosure to mandatory disclosure.

Especially in the initial stage after the release of the draft "Basic Guidelines" for comments, priority will be given to the actual voluntary implementation of enterprises. After all conditions are relatively mature, the Ministry of Finance will work with relevant departments to make targeted arrangements on the scope of implementation, mitigation measures, applicability of relevant clauses, and specific connection provisions.