- Current status

2025 marks the 12th anniversary of the "Belt and Road" Initiative proposal and the 10th year since its formal implementation. Green, sustainable, and high-quality development have consistently been core principles guiding the Chinese government's support for enterprises going global. This is reflected not only in the commitment to cease new overseas coal power investments but also in robust support for sustainable financing by Chinese enterprises abroad. For instance, the China-Singapore Green Finance Corridor, launched in 2023, has become a model for supporting bilateral sustainable financial flows.

1.Sustainable financing becomes a key component of oversea financing by Chinese companies and financial institutions

China is now one of the world's largest sustainable finance markets. Data from 2023 to 2025 on oversea bond issuance indicates a steady increase in both overall issuance volume and the proportion of sustainability-labeled bonds[1] of total overseas issuance by Chinese companies. (Exhibit 1) The share of sustainability-linked labeled bonds in total number of bond issuance grew from 5.8% in 2023 to 14% in 2025. Issuance volume reached $34.5 billion in 2025, a nearly 76% increase from the 2023 level[2]. Labeled bonds have become a vital tool for overseas financing by Chinese companies. This contrasts with the global trend for sustainable bonds; according to ICMA data, global sustainable bond issuance fell from $781.7 billion in 2023 to $737.9 billion in 2025, a 17.7% decline from the 2024 peak of $897.1 billion. This divergence highlights the sustained focus and active participation of Chinese enterprises in sustainable finance markets.

Additionally, labeled bilateral or syndicated loans have become a significant component of overseas financing for Chinese enterprises.

Exhibit 1:Overseas bond issuance by Chinese companies (2023-2025)

Financial institutions have consistently been key participants in the overseas sustainable finance market. Concurrently, an increasing number of companies from other sectors are engaging with the labeled bond market. Notably, the share of all labeled bond issuance by the construction and infrastructure companies grew from 27% in 2023 to nearly 50% in 2025. This can be attributed to the relatively clear green transition pathways, strong green policy support, and narrower traditional financing channels for the real estate industry. (Exhibit 2)

Exhibit 2:2023-2025 Labeled bond issuance by industry(%)

Green remains the dominant category for labeled bond issuance. However, with the development and innovation of sustainable finance markets, other label types are emerging, particularly sustainability bonds[3]. These have seen rapid growth over the past three years, with their share of labeled bond issuance increasing from 21% in 2023 to 46% in 2025.(Exhibit 3)

Exhibit 3: Labeled bond issuance by type (2023 - 2025)

2.Macau, Hong Kong, and Singapore are the Primary Hubs for Overseas Financing

Leveraging geographical advantages, liquidity, and regulatory support, Macau, Hong Kong, and Singapore have become the primary platforms for overseas financing by Chinese enterprises. They are expected to remain core hubs for sustainable finance-related activities. (Exhibit 4)

Hong Kong and Macau have long been the preferred offshore financing markets for Chinese enterprises. Since 2024, over 80% of overseas bond issuances and labeled bonds by Chinese entities have been listed on the Hong Kong and Macau stock exchanges. Singapore's importance as a "secondary listing venue" for bonds and labeled bonds issued by Chinese enterprises is growing, consistently maintaining over an 11% share of listings on the Singapore Exchange.

Exhibit 4: Overview of oversea bond listing (2025)

The attractiveness of the Singapore financial market to Chinese enterprises is related to geopolitical shifts and the deepening trade relationship between China and ASEAN. ASEAN has become China's largest trading partner, and Singapore, with its capital flow convenience, cultural affinity, and strategic location, serves as a hot spot for Chinese enterprises expanding into Southeast Asia. Furthermore, the government's policy and financial support for sustainable finance makes it an ideal market for sustainability-related financing.

- Cost and business needs are primary drivers for Overseas Financing by Chinese Entities

1.Financing cost and policy certainty are primary considerations

Financing costs and policy volatility are core determinants of corporate financing channels and methods. In 2026, despite both China and the US being in easing cycles, Sticky core inflation, a resilient labor market, and uncertainty over the future direction of monetary policy in the United States make US dollar financing costs and their trend difficult to predict, increasing interest rate risks and challenges for overseas issuers’ financing plan. In contrast, China's policy path is relatively clear. Based on the 2026 central bank work conference, monetary policy will maintain a “moderate easing”tone. Overall,RMB financing offers cost advantages and predictability, making it more conducive for offshore entities to conduct medium- to long-term financial planning.

2.Localized financing and brand building

"Financing locally for local use" is becoming an important consideration for Chinese enterprises in their internationalization and local brand development efforts. As overseas operations expand, the flexibility and cost advantages of local financing are becoming increasingly apparent. Concurrently, as Chinese enterprises gain greater market share overseas, international investors and financial service providers gain a deeper understanding of their businesses. This enables Chinese enterprises to not only work with overseas branches of Chinese banks, but also establish closer collaborations with local financial institutions and attract international investors. This virtuous cycle further propels Chinese companies’global expansion.

3.Alignment with sustainable financing

In recent years, the global competitiveness of Chinese companies in sectors like renewable energy and new energy vehicles (NEVs) has strengthened significantly, accelerating their overseas expansion. These industries have a natural alignment with sustainability-related themes. Whether it's NEV manufacturers entering the European market or the rapid deployment of solar and wind power in Southeast Asia, these activities contribute significantly to local green transitions. As markets worldwide introduce sustainable finance policies, financial institutions and investors are paying more attention to assets related to green and sustainability.

4.Constraints remain

Rising geopolitical uncertainty complicates long-term financing planning for enterprises. In addition, there remains a scarcity of underlying assets in the market that meet international green or carbon transition standards while also offering high returns. The financing cost reductions associated with sustainable finance markets are diminishing; declining costs of traditional financing methods weaken the incentive for issuers or borrowers to enter the sustainable finance market. Finally, inconsistencies in green or sustainable finance standards and definitions across different markets contribute to complex and costly cross-border certification processes, introducing further uncertainty.

- 2026 Outlook

1.Continued overseas expansion and active oversea financing

Despite geopolitical challenges, the pace of globalization for Chinese enterprises is unlikely to stop. Overseas financing volumes by Chinese entities are expected to maintain a steady growth in 2026. Companies, particularly in the "new infrastructure" [5]sector, will continue to leverage offshore capital markets to support their overseas business development.

2.Sustainable finance remains policy-driven and fragmented

In 2026, labeled financing is expected to remain policy-driven, with geographical divergence becoming more pronounced: Singapore and Hong Kong, leveraging their mature sustainable finance ecosystems and supportive policies, will remain hubs for sustainable financing activities. Conversely, due to geopolitical uncertainties and the Trump administration's negative stance on sustainable finance and ESG, financing difficulty and costs for Chinese enterprises in the US and European markets are likely to increase.

3.Continued innovation in sustainable financing products

(1)Enhanced connectivity between onshore and offshore capital markets, green panda bonds as a potential highlight

According to our data, the cumulative issuance volume in the Panda bond market surpassed RMB 1 trillion in 2025, with the share from purely offshore issuers approaching nearly 50%. In 2026, with the maturation of the Panda bond market and the extension of the temporary tax exemption on interest income for offshore institutions through 2026-2027, the cost advantage of Panda bond financing is expected to amplify. It is anticipated that more sovereign entities from "Belt and Road" countries and multinational corporations will issue Panda bonds. Concurrently, the mutual recognition of domestic and international standards will accelerate, leading more international issuers to issue green Panda bonds that align with both international and domestic standards.

(2)Financial product innovation as a key highlight, transition finance moving from concept to real time cases

As sustainable finance and carbon transition evolve, corporates and financial institutions will continue to explore product innovations. For instance, the Agricultural Bank of China Limited (ABC) Singapore Branch successfully priced and issued its inaugural $300 million, 3-year "Sustainability-Linked Loan financing Bond" (SLLB) in late 2025, representing the first such issuance in Southeast Asia. The issuance attracted peak investor orders of USD2.2 billion and achieved an oversubscription of more than 7 times, underscoring strong investor confidence in the branch's prudent operation and sustainable development strategy.

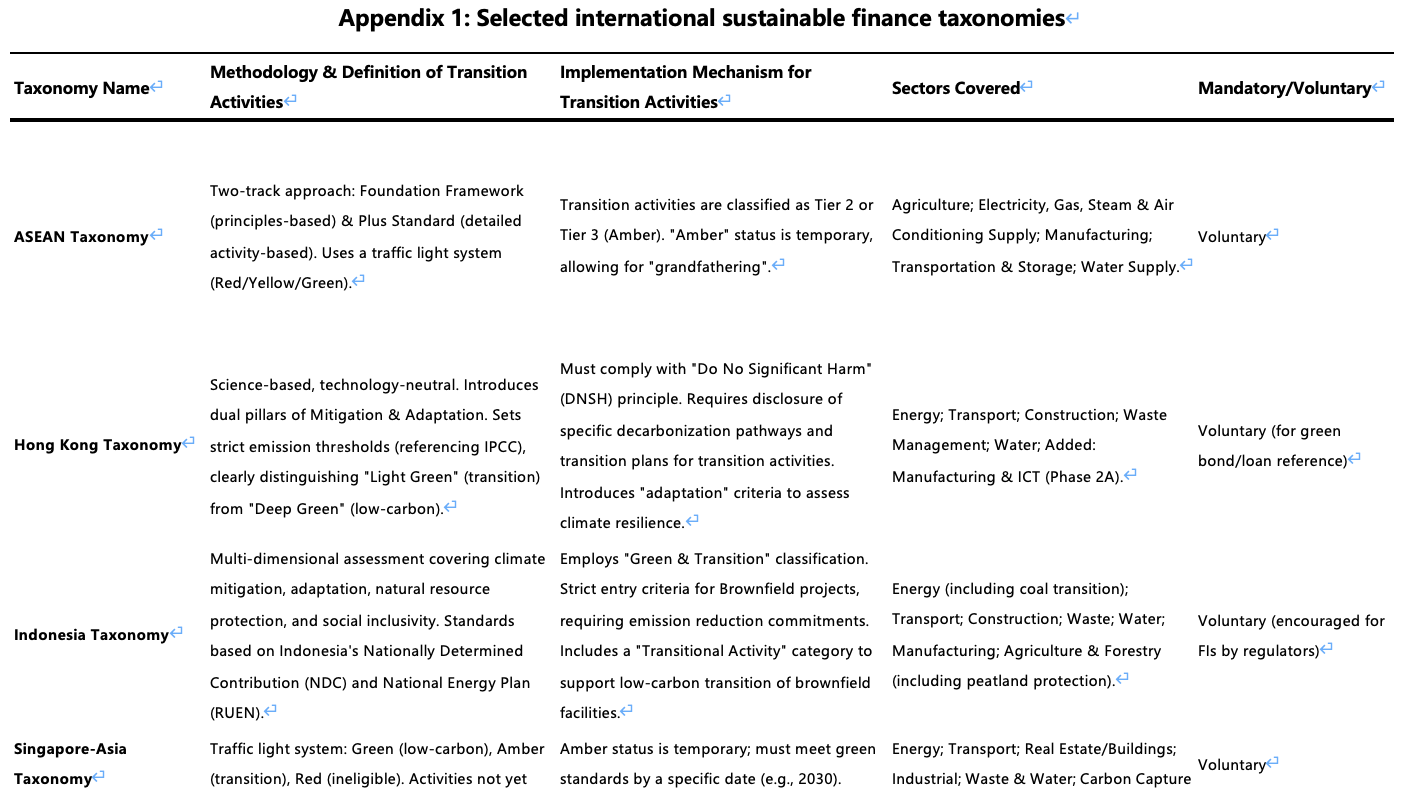

We also expect to see more transition financing cases. China is a leader in this space. We have provided independent second-party opinions for several domestic transition loans and bond issuances by high-carbon-emission enterprises, covering their transition plans and use of proceeds, thereby supporting the orderly transition of these industries. Internationally, major markets are progressively incorporating carbon transition activities into their green or sustainable finance taxonomies (Appendix 1). This will encourage financial institutions in various regions to pay greater attention to the transition needs of high-carbon-emission companies. For example, in late 2025, DBS, Maybank, and OCBC jointly provided a $500 million transition loan to YTL PowerSeraya to build a 600 MW hydrogen-ready gas-fired power plant in Singapore. This represents the nation’s one of the first carbon transition finance transaction cases aligned with Singapore – Asia Taxonomy for Sustainable Finance.

(3)More attention to Multilateral Common Ground Taxonomy

Sustainable finance taxonomies introduced by different markets show distinct local characteristics, covering different sectors and setting varying definitions and thresholds for transition activities. This complexity challenges cross-border labeled financing (Appendix 1). The call from the market for interoperability between national or regional taxonomies is growing stronger. Building on the foundation of the China-EU Common Ground Taxonomy (CGT), efforts by China, the EU, Singapore, and others have led to the development of the Multilateral Common Ground Taxonomy (M-CGT). The M-CGT aims to facilitate cross-border green capital flows and promote standard mutual recognition. Given the rising demand for cross-regional green financing, this taxonomy is expected to garner greater market attention in 2026.

- Conclusion

The overseas financing market for Chinese enterprises in 2026 is expected to expand further. Sustainable financing will become a core element for companies to demonstrate global competitiveness and achieve high-quality development. As a leading provider of sustainable finance solutions, we are committed to promote best practices, and help our clients navigate a complex international environment with stability and foresight.

Appendix 1: Selected international sustainable finance taxonomies

[1] Includes sustainability-labeled bonds such as sustainable, sustainability-linked, green, blue, social, and climate transition finance bonds. "Overseas issuance by Chinese entities" refers to issuances by Chinese issuers conducted outside of Mainland China, including listings on the Hong Kong and Macau stock exchanges.

[2] Source of data: Dealing Matrix International, CCX Trustlink

[3] Sustainability bonds are "Use of Proceeds" bonds directed at green and social projects; Sustainability-Linked Bonds are "General Purpose" bonds whose financial characteristics (e.g., coupon) are tied to the issuer achieving predefined Sustainability Performance Targets.

[4] EU-based exchanges include Frankfurt Stock Exchange, Luxembourg Stock Exchange, Düsseldorf Stock Exchange, EU MTF, Munich Stock Exchange, Vienna Stock Exchange, Boerse Stuttgart, Euronext Paris, and China Europe International Exchange (CEINEX)

[5] Include high-tech, renewable energies, advanced transportation, etc.